- Why LoCorr

A LEADER IN LOW-CORRELATION INVESTMENT SOLUTIONS FOR 20 YEARS

- Investment Solutions

- Insights & Education

- Literature

Is the U.S. economy now in a recession or are the fears of a recession still just circling? While two consecutive quarters of negative gross domestic product (GDP) usually indicates the economy has entered a recession, the actual decision could come months from now when the National Bureau of Economic Research makes the determination. Of course, considering rising interest rates, raging inflation, and record-high gas prices, recessionary concerns were not unexpected. Despite the uncertainty, one thing seems likely: the next ten years will look different from the previous ten.

Substantial and prolonged quantitative tightening is not something we’ve seen in recent history. It will likely mean volatility will become more commonplace in financial markets—and be sustained over longer periods. This means to reach financial goals, financial professionals should think more carefully about portfolio construction and what may best serve investors heading into the next ten years.

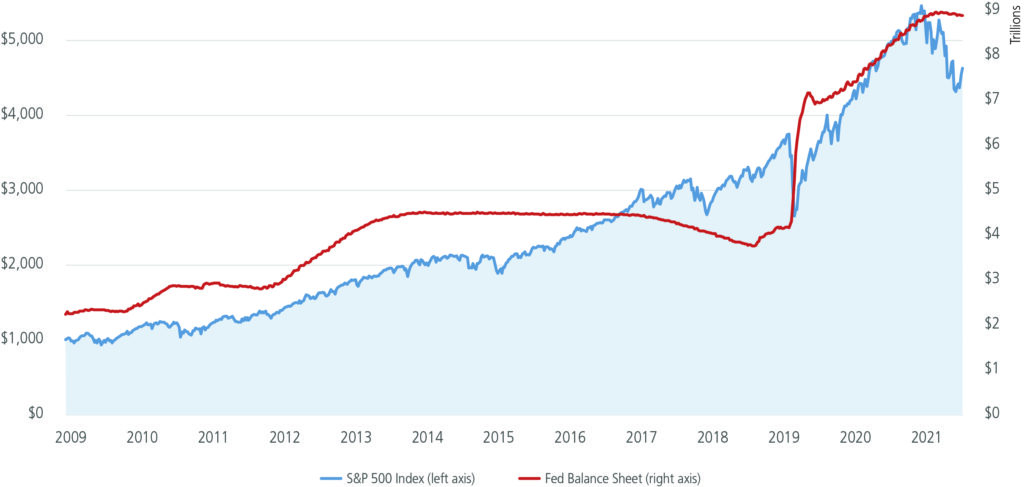

Following the stock market crash in 1987, when Alan Greenspan was the chair of the Federal Reserve, he set a precedent that the Fed would intervene in the domestic markets in times of crisis. Nicknamed the “Fed put” or the “Greenspan put,” the Fed would promptly inject liquidity into the market by purchasing trillions of dollars of U.S. Treasuries after a significant drop in the stock market.

The success of these injections is shown below by the market’s response to the easing of the Fed’s balance sheet.

Source: currentmarketvaluation.com. Table data is since 1/1/2010-6/30/2022.

Such a stance on quantitative easing helped investors feel like they could take on more risk, knowing the Fed would likely throw a lifeline before the risk became too great. This created an artificial market environment performing differently than historical markets and unwittingly created a false sense of security for investors. The unchartered territory of this environment provided years of unprecedented equity growth and left investors feeling confident—perhaps too confident—about the market and their high-risk portfolios.

Coming out of the pandemic with the U.S. economy reopening and stimulus money abounding, the Fed announced plans to begin tightening its belt. Many are unsure of what quantitative tightening will look like over the long term or the effect that the Fed’s quicker-than-historical tightening will have on the market, but the anticipation of quantitative tightening has quickly led to increased volatility in the market.

In March of this year, the Fed made its first rate hike since 2018 of 25 basis points with plans to make additional hikes throughout the year and into next. As inflation continued to rise, the Fed announced its intention to bump interest rates by 50 basis points at each of the future meetings. However, with inflation moving higher than anticipated, the Fed chose to raise rates by 75 basis points at both its June and July meetings; these were the third and fourth rate hikes this year, with June’s hike being the largest increase since 1994. Whether this aggressive stance will help stave off inflation or not is yet to be seen. We believe, however, that given the end of this artificially propped-up environment, investors should reconsider how they construct portfolios going forward, particularly how to add greater diversification to a traditional 60/40 portfolio.

Many believe the current market resembles the 1970s and early 1980s when inflation and gas prices rocketed to record highs. However, this time could be different. For starters, part of today’s high inflation is a result of pandemic disruptions. As the U.S. started to come out of the pandemic, there was high demand for goods from consumers armed with stimulus checks and hefty savings accounts. Factor in supply chain slowdowns and bottlenecks caused by lingering pandemic shutdowns globally, and you get inflationary pressure. While the Fed’s main policy tools are interest rates and asset purchases, these are blunt instruments and not designed to target nor quickly solve global pandemics or supply chain disruptions. In addition, much has been learned about inflation and its long-standing impact on the market since the ‘70s. Today’s Fed seeks to be different by being more transparent with its intentions, providing signals to the markets and the public.

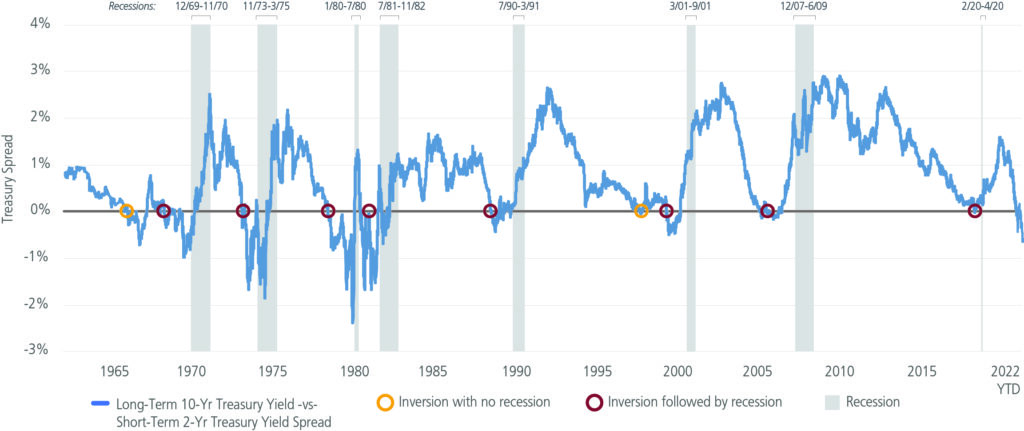

As inflation has continued its rapid ascent, recession concerns have been building. While the academic definition of a recession calls for two-quarters of negative GDP growth, many subscribe to other recession indicators, such as yield curve inversions, real income, employment, industrial production, and retail sales. If you explore the first indicator, yield curve inversion, then you might be in the camp that a recession is coming. As you can see below, historically, a recession has followed a yield curve inversion 80% of the time.

Sources: FRED, NBER (for economic recession data)

Since January 1962, there have been ten periods of yield curve inversion. In eight of those periods, the inversion was followed by an economic recession within 13.6 months, on average.

| Yield Curve Inversion Date | Months to Recession |

|---|---|

| April 11, 1968 | 19 months |

| March 9, 1973 | 7 months |

| August 18, 1978 | 16 months |

| September 12, 1980 | 9 months |

| December 13, 1988 | 18 months |

| February 2, 2000 | 12 months |

| December 27, 2005 | 23 months |

| August 27, 2019 | 5 months |

Sources: FRED, NBER (for economic recession data)

The most recent yield curve inversions happened on April 1, 2022, and again in July of this year. Also, the yield curve inversion between 10-year and 2-year rates reached its largest point since 2000 on July 12. Does that mean a recession is imminent? That remains to be seen.

Another common recession indicator is retail sales. Several big retailers have recently reported high inventory levels and lower demand. As a result, a few retailers have announced downward revisions to margin forecasts for the second quarter of 2022. This indicates consumers are being careful with their spending and spending less. It also means these retailers are under pressure to reduce their current inventory, potentially at deep discounts, to make space for the upcoming holiday season inventory.

However, in discord to the negative indicators, employment remains strong. In June, non-farm payroll employment rose, while the unemployment rate remained unchanged at historically low levels, according to the U.S. Bureau of Labor Statistics. This makes the current environment unique. In the past, each time the market has gone into a recession, unemployment has risen substantially, as GDP decreased. As we stand now, this is not the case, making the current environment appear different.

Whether the indicators point to a recession or not, the key to market uncertainty is always being prepared—in good times and bad. This means proper diversification should be a constant mindset, not a reaction. Investors must look for other sources of return that can provide diversification beyond stocks and bonds.

Managed Futures is one such strategy. Known for its low correlation to nearly all asset classes, differentiated return stream, and ability to provide crisis alpha, Managed Futures are a worthy alternative to fixed income. These strategies have shown strong historical performance when stocks have suffered, especially in recessionary periods.

Another option to consider is to blend different strategies that are uncorrelated to stocks and bonds. Diversifying a portfolio with these strategies has the potential to both mitigate risk and improve long-term returns. By combining low-correlating strategies, this sleeve of the portfolio can deliver a more consistent return stream and provide a smoother ride across multiple market cycles—including uncertain ones—creating an investor experience with better outcomes and less volatility.

Can I still adjust my allocation to include alternatives in my portfolio or have I missed the boat? We’ve been asked this question a lot lately...

Read MoreDespite the uncertainty, one thing seems likely: the next ten years will look different from the previous ten....

Read MorePortfolios need opportunities for growth and diversification. The time may be right to rec...

Sign in to Read MoreDiversification does not assure a profit or protect against loss in a declining market. Correlation measures how much the returns of two investments move together over time. Drawdown refers to how much an investment or trading account is down from the peak before it recovers back to the peak. Drawdowns are typically quoted as a percentage, but dollar terms may also be used if applicable for a specific trader. Drawdowns are a measure of downside volatility. Alpha measures the difference between an actual return for a stock or a portfolio and its equilibrium expected return.

S&P 500 Index is a capitalization weighted unmanaged benchmark index that includes the stocks of 500 large capitalization companies in major industries. This total return index includes net dividends and is calculated by adding an indexed dividend return to the index price change for a given period.

Past Performance does not guarantee future results. Index performance is not indicative of fund performance.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 1.855.LCFUNDS, or visiting www.LoCorrFunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible.

The Funds are non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Funds are more exposed to individual stock volatility than a diversified fund. The Funds invest in foreign investments and foreign currencies which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investing in commodities may subject the Funds to greater risks and volatility as commodity prices may be influenced by a variety of factors including unfavorable weather, environmental factors, and changes in government regulations.

Investing in derivative securities derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks, and, depending upon the characteristics of a particular derivative, suddenly can become illiquid. Derivative contracts ordinarily have leverage inherent in their terms which can magnify the Fund’s potential for gains or losses through increased long and short position exposure. The Fund may access derivatives via a swap agreement. A risk of a swap agreement is the risk that the counterparty to the agreement will default on its obligation to pay the Fund.

Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset Backed, Mortgage Backed, and Collateralized Mortgage-Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments.

The LoCorr Dynamic Equity Fund may invest in small- and medium-capitalization companies which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in lower-rated and non-rated securities which present a greater risk of loss to principal and interest than higher-rated securities. ETF investments are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are subject to specific risks, depending on the nature of the ETF.

The Spectrum Income Fund’s portfolio will be significantly impacted by the performance of the real estate market generally, and the Fund may be exposed to greater risk and experience higher volatility than would a more economically diversified portfolio. Property values may fall due to increasing vacancies or declining rents resulting from economic, legal, cultural, or technological developments. Investments in Limited Partnerships (including master limited partnerships) involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the Limited Partnership, risks related to potential conflicts of interest between the Limited Partnership and the Limited Partnership’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. Underlying Funds are subject to management and other expenses, which will be indirectly paid by the Fund.

Click here for important disclosure and definition information.

Mutual fund investing involves risk. Principal loss is possible. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by clicking here or a free-hard copy is available by calling 1.855.LCFUNDS. Read it carefully before investing. The Funds are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy or an offer to sell shares of the Funds in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction. The LoCorr Funds are distributed by Quasar Distributors, LLC.

If you have previously created a password protected account from LoCorr Funds, please sign in below to view gated materials.

Please enter your company email address. You will receive an email message with instructions on how to reset your password.

Send Recovery EmailThank you. A password reset email will be sent to you soon.