- Why LoCorr

A LEADER IN LOW-CORRELATION INVESTMENT SOLUTIONS FOR 20 YEARS

- Investment Solutions

- Insights & Education

- Literature

While advisors may be cautiously optimistic about elevated bond yields, it is crucial to consider the other important reason for investing in bonds beyond return and income, and that is diversification. Bonds have historically played a significant role in diversifying portfolios, which has led to reduced overall volatility, and has been a hedge against equity market fluctuations. In the current landscape, where bonds and stocks are experiencing a period of positive correlation, it becomes even more important (if not critical) to incorporate additional diversification strategies to help mitigate portfolio risk and preserve portfolio balance.

In this article, we delve into the historical role of bonds for potential return and diversification benefits, the impact of changing dynamics on bonds’ ability to deliver on these expectations, and the importance of including additional diversifiers to possibly help compensate for periods of positive correlation (which happen more often than you think). We also explore the potential benefits of incorporating a sleeve of low-correlating assets to help reduce risk and enhance reward in portfolios over multiple market cycles.

By examining bonds’ historical return profile, we can understand the significant contribution bonds have made to overall portfolio performance both in the short and long term. One of the key benefits of bonds is their ability to generate income, historically making them a reliable source of cash flow. Additionally, bonds have the potential to appreciate in value when interest rates decline.

Another potential advantage of bonds is their role in diversification and risk reduction. Traditionally, bonds have shown negative correlation with stocks, meaning they often move in the opposite direction. This inverse relationship has helped to stabilize portfolios during equity market downturns, which has provided a buffer against losses.

This potential combination of stability, capital appreciation, and diversification makes bonds a valuable component of a well-rounded investment portfolio.

The dynamics between stocks and bonds, however, have evolved in recent times. Likely a hidden risk to many investors, we examine the challenges of positive correlation between stocks and bonds and its implications for diversification. Positive correlation implies when stocks rise, bonds also tend to rise, and vice versa. Positive correlation regimes disrupt the traditional diversification benefits of bonds, and during such periods, investors effectively hold a long-only portfolio. An unintended risk.

Source: LoCorr Fund Management and Morningstar Direct. Monthly data as of March 31, 2023. *Average 3-yr rolling correlation between S&P 500 PR Index and 10-Year Treasury Maturity Bond Index.

As advisors understand the need for diversification, it is vital, therefore, to recognize the limitations of relying solely on bonds for balance across all time periods. To offset the inconsistent diversification value of bonds, we believe alternatives, or low-correlating strategies, should be explored.

Low-correlating assets exhibit a lower or non-existent correlation with traditional asset classes like stocks and bonds. By incorporating low-correlating assets into portfolios, investors can potentially achieve improved diversification and risk management, even when stocks and bonds move in tandem.

Correlation ranges on a scale from 1 (perfectly correlated) to -1 (inversely correlated). For advisors whose primary objective is diversification, an optimal correlation value might range between -0.5 to 0.5. Anything below -0.5 has high inverse correlation and anything above 0.5 could move too closely in tandem with equity markets. The objective of diversification is to find strategies that move independently, but not necessarily inversely.

By incorporating low-correlating assets into portfolios, investors can potentially improve diversification and risk management, even when stocks and bonds move in tandem.

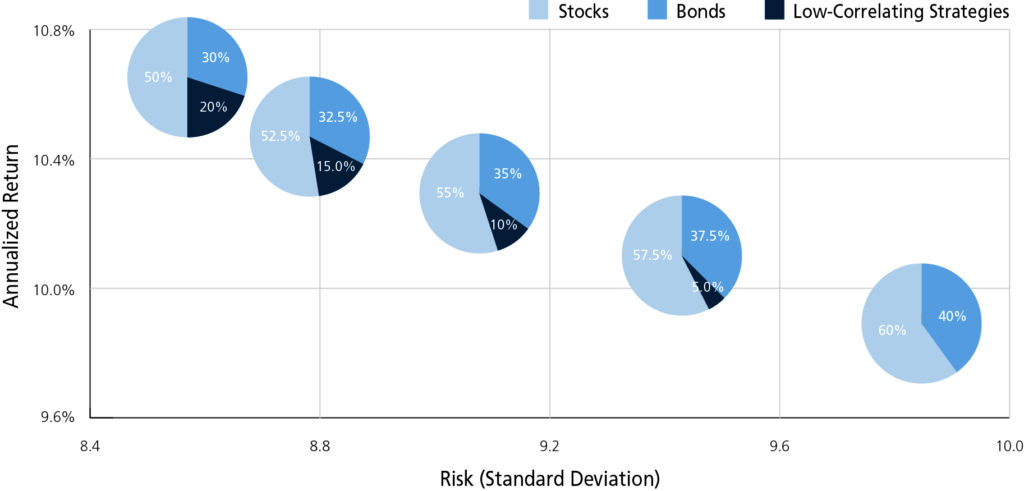

To achieve a better alignment between risk/return objectives using low-correlating assets, we believe combining two or more of these low-correlating strategies into a portfolio, creating what is known as a “sleeve”, can be an effective way to diversify a portfolio.

A sleeve strategy involves the creation of a separate allocation within the portfolio specifically dedicated to low-correlating assets. By doing so, investors can potentially mitigate risks associated with traditional asset classes and the periods of positive correlation to improve diversification. This strategic approach helps balance the risk and reward dynamics, potentially providing a more stable foundation for long-term investment success.

Source: Morningstar Direct. Stocks are represented by the S&P 500 TR Index. Bonds are represented by the Bloomberg U.S. Aggregate Bond Index. Alternatives are represented by the CISDM CTA Equal Weighted Index. Past Performance does not guarantee future results.

The success of a sleeve strategy relies on selecting low-correlating assets to complement the existing portfolio. These assets can vary widely and may include alternative strategies such as bond alternatives, commodities, or strategies like managed futures. Targeting desired outcomes for sleeve composition allows investors to tailor their portfolios to specific risk profiles and investment objectives—such as hedging inflation, or capturing additional return sources, for example.

Diversification remains a fundamental principle of portfolio management, particularly in an increasingly uncertain market landscape. While bonds continue to serve an essential role in portfolios, their potential diversification benefits can be undermined during periods of positive correlation with stocks.

An alternative sleeve strategy may provide a compelling solution by incorporating low-correlating assets with the potential to enhance risk management, reduce portfolio volatility, and improve long-term performance.

To successfully navigate the future, investors and advisors must adapt their investment strategies to manage risk more effectively and to achieve their financial goals, regardless of the market environment. By evolving portfolio construction beyond traditional investments such as stocks and bonds, a more resilient portfolio is possible, one that is capable of better navigating uncertainty, paving the way for a more positive investment outcome in an ever-changing investment landscape.

We believe the traditional 60/40 allocation may now be working against investors...

Read MoreGiven the wide range of economic uncertainties, investors should consider a more diversified asset allocation than 60/40....

View ChartWhen the market is turbulent, investors may be motivated to look for new ways to diversif...

Sign in to Read MoreDiversification does not assure a profit or protect against loss in a declining market. Correlation measures how much the returns of two investments move together over time. Standard Deviation is the statistical measurement of dispersion about an average, which depicts how widely a portfolio’s returns varied over a certain period of time. When a portfolio has a high standard deviation, the predicted range of performance is wide, implying greater volatility.

Bloomberg Capital U.S. Aggregate Bond Index is the most common index used to track the performance of investment grade bonds in the United States. S&P 500 Index is a capitalization weighted unmanaged benchmark index that includes the stocks of 500 large capitalization companies in major industries. This total return index includes net dividends and is calculated by adding an indexed dividend return to the index price change for a given period. 10-Year Treasury Constant Maturity Bond Index is an index published by the Federal Reserve Board based on the average yield of a range of Treasury securities, all adjusted to the equivalent of a 10-year maturity. CISDM CTA Equal Weighted Index is designed to broadly represent the performance of all CTA programs in the Morningstar database that meet the inclusion requirements. S&P 500 Price Return Index is a capitalization weighted unmanaged benchmark index that includes the stocks of 500 large capitalization companies in major industries. This price return index includes net dividends and is calculated by adding an indexed dividend return to the index price change for a given period.

Past Performance does not guarantee future results. Index performance is not indicative of fund performance. For current standardized fund performance, please call 1.855.LCFunds or visit www.LoCorrFunds.com. The performance of various indices is shown for comparison purposes only. The performance of those indices was obtained from published sources believed to be reliable, but which are not warranted as to accuracy or completeness. Unless noted otherwise, index returns do not reflect fees or transaction costs and reflect reinvestment of net dividends. One cannot invest directly in an index.

The Fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 1.855.LCFUNDS, or visiting www.LoCorrFunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. The Funds are non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Funds are more exposed to individual stock volatility than a diversified fund. The Funds invest in foreign investments and foreign currencies which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. The Funds may make short sales of securities, which involves the risk that losses may exceed the original amount invested. Investing in commodities may subject the Funds to greater risks and volatility as commodity prices may be influenced by a variety of factors including unfavorable weather, environmental factors, and changes in government regulations. Investing in derivative securities derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks, and, depending upon the characteristics of a particular derivative, suddenly can become illiquid. Derivative contracts ordinarily have leverage inherent in their terms which can magnify the Fund’s potential for gains or losses through increased long and short position exposure. The Fund may access derivatives via a swap agreement. A risk of a swap agreement is the risk that the counterparty to the agreement will default on its obligation to pay the Fund. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in Asset Backed, Mortgage Backed, and Collateralized Mortgage-Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. The LoCorr Dynamic Equity Fund may invest in small- and medium-capitalization companies which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in lower-rated and non-rated securities which present a greater risk of loss to principal and interest than higher-rated securities. ETF investments are subject to investment advisory and other expenses, which will be indirectly paid by the Fund. As a result, the cost of investing in the Fund will be higher than the cost of investing directly in ETFs and may be higher than other mutual funds that invest directly in stocks and bonds. ETFs are subject to specific risks, depending on the nature of the ETF. The Spectrum Income Fund’s portfolio will be significantly impacted by the performance of the real estate market generally, and the Fund may be exposed to greater risk and experience higher volatility than would a more economically diversified portfolio. Property values may fall due to increasing vacancies or declining rents resulting from economic, legal, cultural, or technological developments. Investments in Limited Partnerships (including master limited partnerships) involve risks different from those of investing in common stock including risks related to limited control and limited rights to vote on matters affecting the Limited Partnership, risks related to potential conflicts of interest between the Limited Partnership and the Limited Partnership’s general partner, cash flow risks, dilution risks and risks related to the general partner’s limited call right. Underlying Funds are subject to management and other expenses, which will be indirectly paid by the Fund.

The LoCorr Funds are distributed by Quasar Distributors, LLC. © 2023 LoCorr Funds

If you have previously created a password protected account from LoCorr Funds, please sign in below to view gated materials.

Please enter your company email address. You will receive an email message with instructions on how to reset your password.

Send Recovery EmailThank you. A password reset email will be sent to you soon.